Reports .3B Q4 2025 Revenue with Strong Software, Services Profitability")

Taiwan Semiconductor will be a huge winner as long as AI spending continues.

With the four major AI hyperscalers set to spend around $650 billion in 2026 on data center capital expenditures, there are a lot of companies slated to cash in. While some may question how much Amazon, Microsoft, Alphabet, and Meta Platforms are spending, the reality is that AI demand is real, and any company not spending as much as they can to establish a foothold in this industry is falling behind.

There are several ways to play this spending, but my favorite, by far, is Taiwan Semiconductor (TSM +2.82%). Taiwan Semiconductor is slated to be a winner regardless of which computing unit is used, making it a no-brainer buy right now.

Image source: Getty Images.

Chip foundries are far and few between

There are only a handful of chip companies that can even compete with Taiwan Semiconductor. Intel (INTC 1.22%) used to be one of them, but its chip foundry business has fallen on hard times and is struggling to compete with TSMC. Furthermore, with Taiwan Semiconductor building factories on U.S. soil, it’s becoming even less of an attractive option. Another pick is Samsung. Samsung’s capabilities are better than Intel’s, but it just doesn’t have nearly the capacity to compete with Taiwan Semiconductor.

Taiwan Semiconductor Manufacturing

Today’s Change

(2.82%) $10.15

Current Price

$370.54

Key Data Points

Market Cap

$1.9T

Day’s Range

$359.10 – $372.20

52wk Range

$134.25 – $380.00

Volume

9M

Avg Vol

13M

Gross Margin

59.02%

Dividend Yield

0.83%

That leaves it as really the only option available, which is why Taiwan Semiconductor’s client list includes massive players like Nvidia, AMD, and Broadcom. Regardless of whether one of these four hyperscalers is filling their data center with graphics processing units (GPUs) from Nvidia, or maybe a custom-designed chip from Broadcom, the odds are high that the chip originated from one of Taiwan Semiconductor Manufacturing’s facilities.

This makes Taiwan Semiconductor the neutral way to play the AI buildout, as it’s set to make a fortune as long as AI spending continues. And from management’s view, it could be some time before AI spending slows down.

Taiwan Semiconductor’s management noted that between 2024 and 2029, they expect AI chip revenue to grow at nearly a 60% compound annual growth rate (CAGR). That’s huge growth, and showcases the size and longevity of the AI buildout that’s still going on.

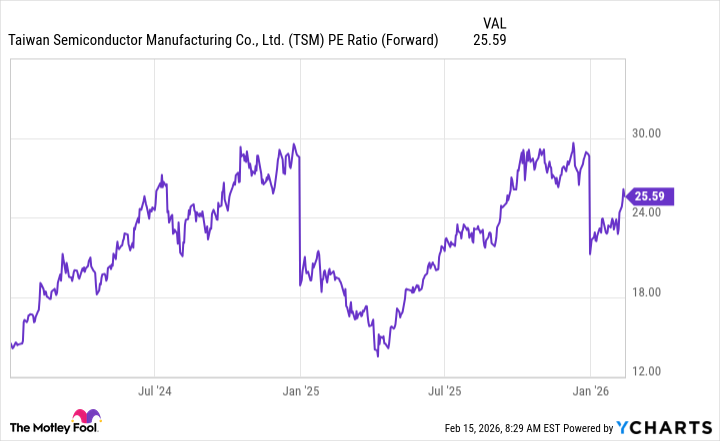

Despite all of the massive projects for huge AI spending growth, Taiwan Semiconductor’s stock isn’t valued at a massive premium.

TSM PE Ratio (Forward) data by YCharts

With the stock trading for 26 times forward earnings, it’s not that much more expensive than the S&P 500 (^GSPC +0.69%), which is priced at 22 times forward earnings. While the stock isn’t as cheap as it used to be, it’s still an excellent one to buy now, as it’s a great way to play the AI buildout.

Keithen Drury has positions in Alphabet, Amazon, Broadcom, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Intel, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Reports First Year of Net Profitability and 19% Q4 Revenue Growth")

Plans?")

Outperform on Pentagon Missile Manufacturing Framework Deal")