Alphabet (GOOG 1.42%) (GOOGL 1.43%) has staged a massive comeback over the past year. If you bought shares at this time last year, you’re up around 70% on your investment. With that kind of one-year return, it’s logical to wonder if Alphabet’s stock still has room for upside.

I think there’s still a strong case to buy Alphabet’s stock right now, and if you’ve missed out on the massive run, there still may be time for you to get in.

Image source: The Motley Fool.

1. Alphabet has emerged as a top option in AI

A year ago, Alphabet was the laughing stock of the generative AI world. Now, it’s among the leaders. Alphabet has one advantage that many of the other generative AI makers don’t: a side business. The other AI companies are deeply unprofitable and require outside investments to continue running. Alphabet can self-fund its AI wing through its other businesses, including Google Search, YouTube, and Google Cloud, among many others.

Although there is fierce competition going on, Alphabet’s models are right there with the best, and it may be able to price its tokens lower than its peers due to being able to absorb the costs. This could give Alphabet a leg up on its competition when it comes to which model will be the most dominant, but we’re still years away from learning what the final result will be.

Still, Alphabet has won a key customer: Apple. Apple will use Gemini to run its next iteration of Siri that utilizes generative AI. This is a lucrative customer base, and for Alphabet to win this battle showcases that it’s a top option.

Today’s Change

(-1.43%) $-4.40

Current Price

$304.30

Key Data Points

Market Cap

$3.7T

Day’s Range

$301.03 – $308.71

52wk Range

$140.53 – $349.00

Volume

937K

Avg Vol

34M

Gross Margin

59.68%

Dividend Yield

0.27%

2. Google Cloud is on fire

Google Cloud is one of the fastest-growing segments within Alphabet. The cloud computing platform is seeing huge demand from AI workloads, and the cloud computing business model has proven to be a successful one, as AI developers are renting computing power rather than building their own.

Furthermore, Google Cloud grants its clients access to its TPUs, an alternative to more expensive GPU hardware. Businesses are looking to cut costs wherever possible. If they can get similar results by running workloads on TPUs instead of GPUs, Alphabet is primed to capitalize on huge growth.

During Q4, Google Cloud posted an incredible 48% year-over-year growth rate. It’s also doing it in a profitable manner, with its operating margin coming in at 30%. Google Cloud should continue to be a highlight for Alphabet’s business, and its continued success showcases that its cloud platform will continue to be a top option to buy AI models on.

3. Alphabet’s valuation is reasonable

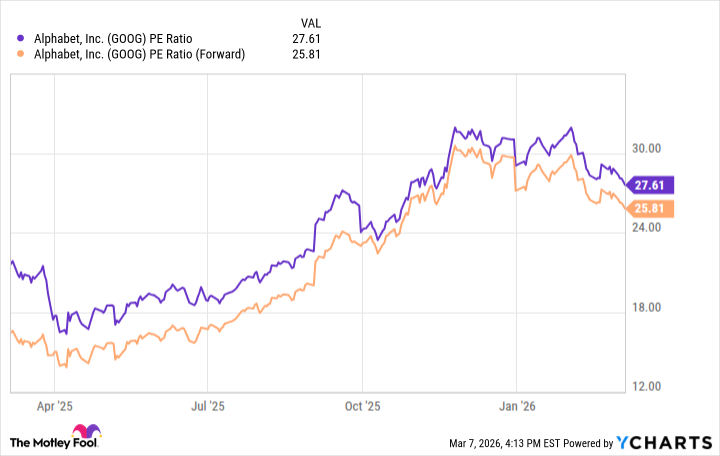

A year ago, you could have bought Alphabet’s stock for about 16 times forward earnings. Those days are long gone, and now Alphabet trades for about 26 times forward earnings and 28 times trailing earnings.

GOOG PE Ratio data by YCharts

While that’s not a screaming bargain valuation, it’s also not a bad price to pay. For reference, the S&P 500 trades for about 21.7 times forward earnings and 24.6 times trailing earnings. That only prices Alphabet’s stock a few points above the market, and with Alphabet’s strong track record and bright future, that premium valuation is earned.

With Alphabet’s stock selling off quite a bit over the past month, I think now is the perfect opportunity to get into the stock at a much better valuation. Alphabet has established itself as an AI leader, and it’s not often you can buy leaders in emerging industries at a discount to where they previously traded. As a result, Alphabet looks like a top-tier buy in March.