The U.S. is home to nine American companies worth $1 trillion or more, but as I write this, only three are in the ultra-exclusive $3 trillion club:

- Nvidia: $4.2 trillion.

- Apple: $3.6 trillion.

- Alphabet: $3.6 trillion.

I predict Meta Platforms (META 1.91%) will join them within the next three years. The company is using artificial intelligence (AI) to boost engagement on its Facebook and Instagram social media applications, which is driving more advertising revenue.

Meta has a market capitalization of $1.5 trillion as I write this, so investors who buy its stock today could double their money if it does join the $3 trillion club.

The Meta Platforms logo. Image source: The Motley Fool.

AI is transforming the social media experience

According to the company, nearly 3.6 billion people use at least one of Meta’s social media apps every single day, which is close to half the entire global population. For that reason, it’s becoming harder for the company to find new users, which threatens the long-term potential of its business. As a result, management is focusing on boosting engagement instead — if users spend more time on Meta’s apps each day, they will see more ads, which leads to more revenue.

AI is central to that strategy. Advanced algorithms learn what type of content each user likes to see on Facebook and Instagram, and it feeds them more of it to keep them online for longer periods of time. It’s working like a charm; during the third quarter of 2025 (ended Sept. 30), for example, AI-driven recommendations drove a 30% year-over-year increase in the amount of time users spent watching Instagram Reels (videos).

And this is only the beginning. CEO Mark Zuckerberg believes all users will eventually have their own AI agent that learns about their personal interests over time and curates their entire social media experience. The agent will also be capable of creating content for users to post or share with friends, which could drive an increase in activity.

Lastly, agents could also transform social media for advertisers. Since they will have such a deep understanding of each user, they could significantly improve Meta’s ability to sell highly targeted ads. If this increases conversions for businesses, the company can charge more money for every advertising slot.

Meta is forecasting a record year of AI capital expenditures

Meta delivered a record $200.9 billion in revenue during 2025, which was up 22% from the previous year. The company’s net income came in at $25.4 billion, representing a small decline of 3% due to a large, one-off tax provision related to the Trump administration’s so-called Big Beautiful Bill. However, if we exclude the provision, Meta’s net profit would have grown by around 20% to over $74 billion instead.

Today’s Change

(-1.91%) $-11.55

Current Price

$592.51

Key Data Points

Market Cap

$1.5T

Day’s Range

$591.00 – $600.54

52wk Range

$479.80 – $796.25

Volume

668K

Avg Vol

14M

Gross Margin

82.00%

Dividend Yield

0.35%

Meta could be making even more money right now, but its bottom line faces two major headwinds: First, the company’s enormous AI-related capital expenditures (capex), which soared by 84% to a record $72.2 billion in 2025. The AI data center infrastructure and chips purchased with that money get depreciated over several years, so while the up-front cost doesn’t hurt the bottom line immediately, it becomes a drag on Meta’s profitability over the long term.

And second are the significant operating losses in the Reality Labs division, which is home to the company’s metaverse and virtual reality projects. The segment lost a staggering $19.2 billion during 2025.

Meta recently announced plans to wind down some of its metaverse ambitions, given the lack of traction and revenue, which should narrow Reality Labs’ losses during 2026. However, the company says its AI-related capex will soar to somewhere between $115 billion and $135 billion this year, which could result in sluggish earnings growth in the years to come.

But as I touched on earlier, these investments in AI are yielding a significant increase in user engagement across Meta’s social media apps, so the company’s revenue probably wouldn’t be growing as fast right now without them. In other words, there could be an enormous long-term return on every dollar Meta funnels into AI today.

The mathematical path to the $3 trillion club

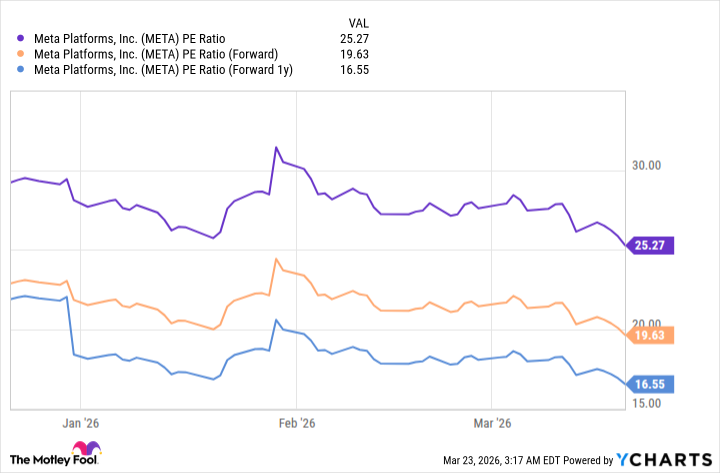

Based on Meta’s earnings of $23.49 per share, its stock is trading at a price-to-earnings ratio (P/E) of just 25.3. That is a notable discount to the Nasdaq-100 index, which trades at a P/E of 30, suggesting Meta might be undervalued relative to its big-tech peers.

Despite the challenges facing the company’s bottom line, Wall Street thinks earnings will grow to $29.60 per share in 2026, and then $34.39 per share in 2027 (according to Yahoo! Finance), placing its stock at forward P/E ratios of 19.6 and 16.5, respectively.

Data by YCharts; PE = price to earnings.

If we assume Wall Street’s forecasts prove to be accurate, Meta stock will have to soar 82% by the end of 2027 just for its P/E to match the current figure for the Nasdaq-100 — which isn’t out of the question given Meta’s P/E was over 30 just six months ago. This would catapult the company’s market cap to $2.73 trillion.

That means Meta would have to grow its earnings by just 10% in 2028 to justify a market cap of $3 trillion. However, if Wall Street’s forecasts for 2028 look much stronger, investors might start pricing in some of the upside in 2027, which could help the company achieve the valuation milestone even sooner.

In any case, I think it’s only a matter of time before Meta sits alongside other tech titans like Nvidia in the $3 trillion club.