in Q4")

Growth stocks are under pressure as investors question the payoff of aggressive spending plans.

As of market close on Feb. 17, Nvidia, Alphabet, Apple, Microsoft, Amazon, Meta Platforms (META +0.72%), and Tesla (TSLA 2.17%) were all down more than the S&P 500 year-to-date. The group, collectively known as the “Magnificent Seven,” has been instrumental in driving the index’s gains in recent years.

Investors looking to buy the dip on Magnificent Seven stocks have come to the right place. Here’s why Meta Platforms stands out as a buy now, and why Tesla could be a buy in the future, but is worth avoiding for the time being.

Image source: Getty Images.

Meta Platforms is a high conviction buy

Cloud computing customers are increasingly relying on compute, storage, and networking capabilities to support high-performance computing and artificial intelligence (AI) workflows. Companies like Amazon Web Services and Microsoft Azure are building out infrastructure to meet demands, but it’s incredibly competitive. Hyperscalers are following up record-high 2025 capital expenditures (capex) with even bolder plans in 2026.

Amazon is forecasting capex to increase 55.9% year over year to $200 billion. Microsoft spent $37.5 billion on capex in its latest quarter — which is more than half of its entire fiscal 2025 capex. Meanwhile, Oracle is under intense pressure due to mounting debt and negative free cash flow as it bets big on surging demand for Oracle Cloud Infrastructure.

Cloud computing giants are depending on sustained demand for their infrastructure, but if demand declines, overcapacity and overinvestment could strain their financial results.

Today’s Change

(0.72%) $4.71

Current Price

$658.40

Key Data Points

Market Cap

$1.7T

Day’s Range

$647.55 – $660.93

52wk Range

$479.80 – $796.25

Volume

612K

Avg Vol

16M

Gross Margin

82.00%

Dividend Yield

0.32%

Meta Platforms has a far simpler approach to AI, which is why it’s one of the best growth stocks to buy now. Meta has several near- and long-term pathways to monetize its AI investments. The company uses AI to improve the user experience across its Family of Apps — Instagram, WhatsApp, Facebook, and Messenger. It also uses AI to better connect advertisers with the right potential customers based on interests.

Thanks to the cash cow ad business, Meta can take the pressure off making money from its longer-term AI endeavors. Meta’s open-source, freely available Large Language Model Meta AI (LLaMA) is built to maximize adoption, which can create long-term network effects. Meta AI assistants, which are built on LLaMA 4, improve content creation and user experiences, offer business tools, and enable task automation.

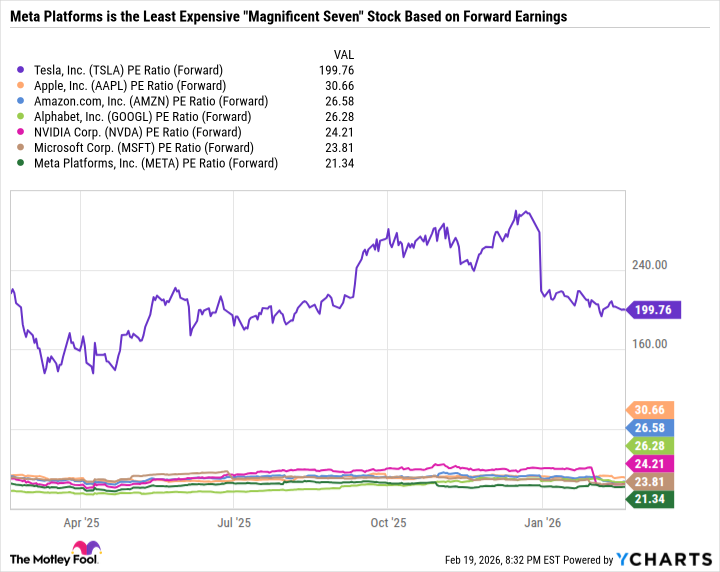

All told, Meta is in a league of its own when it comes to aggressive AI investment without compromising on high margins or cash flow. And at just 21.3 times forward earnings, Meta will appeal to value investors as the least expensive of the Magnificent Seven stocks.

TSLA PE Ratio (Forward) data by YCharts

Tesla has a lot to prove before it’s a buy

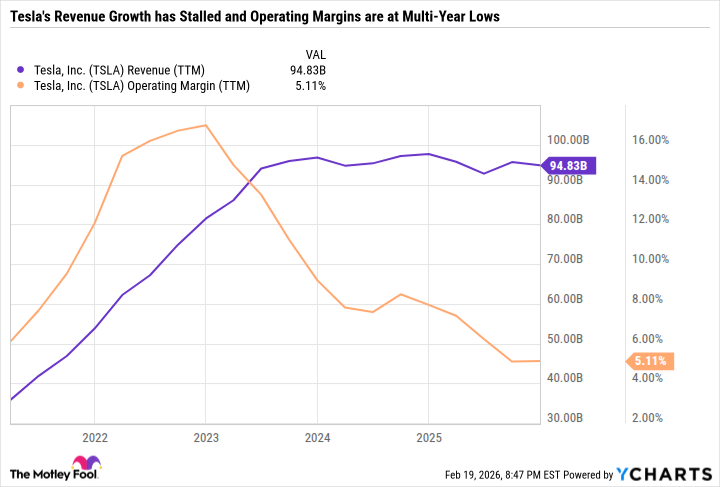

Tesla is worth avoiding for the same reasons why Meta is a buy. Tesla’s former cash cow, its electric vehicle business, is in decline. Although it still holds a considerable global EV market share. Its energy business and services segments are doing quite well, but remain a relatively small portion of the broader company. Tesla’s competitive advantage used to be its industry-leading margins. But now, Tesla’s mid-single-digit margins resemble more of a legacy auto maker than a high-growth company.

TSLA Revenue (TTM) data by YCharts

Given the current state of Tesla, investors may be wondering why the stock is so expensive. That’s because it has multiple, potentially transformative ideas — namely, robotaxis and its Optimus robots.

Instead of depending on people to buy a Tesla EV over an alternative passenger car, the robotaxi flips the business model around by creating a fleet of self-driving, AI-powered vehicles that can reduce car ownership costs and provide alternatives to human-dependent ride-sharing models. Robotaxi is based on existing Tesla models, while the more ambitious Cybercab would be an autonomous-first vehicle without a steering wheel.

Meanwhile, Optimus has the potential to automate workflows in industrial, commercial, and residential settings. Especially early on, integrating Optimus to perform tasks, say, in a warehouse, seems far more likely than widespread adoption of Optimus robots folding laundry. But still, there is no company quite like Tesla, which is why some investors are willing to pay such a premium for the stock.

The challenge, as my colleague Daniel Sparks points out, is execution risk. The adoption and profitability of Tesla’s big ideas are entirely unproven. It also remains to be seen what success even looks like. Tesla sports a market capitalization of $1.55 trillion, which is in the ballpark of Meta’s $1.63 trillion market cap. But Meta raked in over $60 billion in 2025 net income compared to under $4 billion for Tesla.

Tesla is full of potential, but so much has to go right just to justify its existing valuation, let alone provide a decent return for investors considering buying the stock now. Tesla could be worth buying if it proves that robotaxi and/or Optimus can generate consistent earnings growth. But until then, there are far better buys in today’s market.