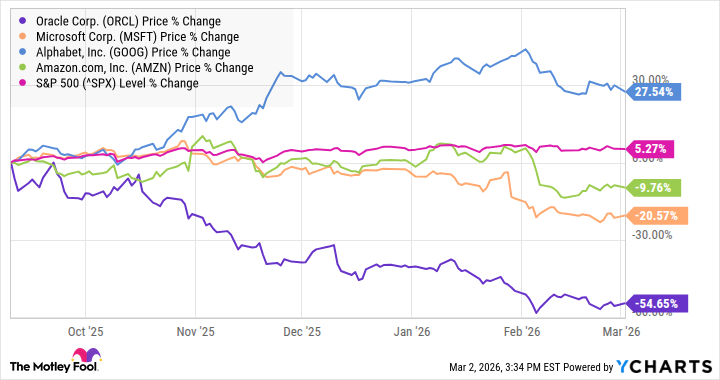

Oracle (ORCL +2.65%) declined 11.7% in March according to data from S&P Global Market Intelligence. The stock is down more than 23% in 2026 as I write. However, the key benchmark date is likely mid-September, when news of the $300 billion deal with OpenAI broke. The initial euphoria over the deal quickly faded, and Oracle’s stock is down more than 54% since mid-September.

Image source: Getty Images.

OpenAI and Oracle

The chart below shows Oracle’s decline, and it’s no coincidence that Microsoft (whose cloud computing business, Azure, has 45% of its backlog coming from OpenAI) is also a significant underperformer, while Alphabet (with minimal OpenAI exposure) is the outperforming hyperscaler.

ORCL data by YCharts

Moreover, it’s not just equity market investors who are uncomfortable with Oracle’s exposure to the loss-making and highly cash-burning OpenAI, because bond investors have pushed Oracle’s 5-year credit default swap (CDS) spread pricing to about 120 basis points to 150 basis points (where 100 basis points equals 1%) from less than 50 basis points before the OpenAI deal.

CDS spreads represent the price to protect against a default. For reference, Alphabet’s 5-year CDS are about 45 basis points

Funding the AI rollout

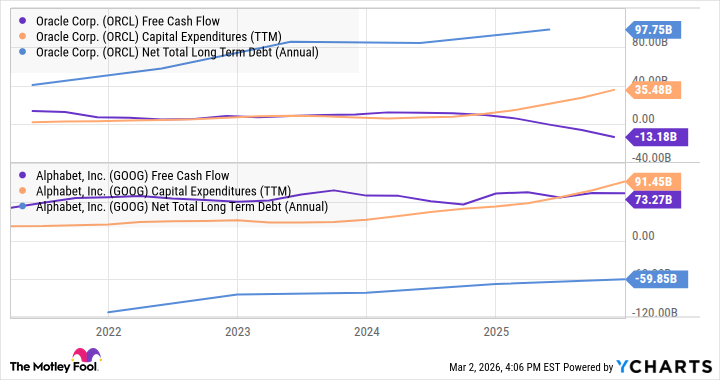

The difference between Alphabet and Oracle is even clearer when comparing Oracle’s ballooning debt, cash outflows, and capital spending commitments with Alphabet’s much more favorable position.

ORCL Free Cash Flow data by YCharts

It’s not just a question of Oracle’s financial position and ability to fund AI investment commitments; the market is also worried about OpenAI’s ability to secure funding and ultimately achieve the profitability needed to buy services from Oracle.

Those fears weren’t helped much by Nvidia only committing $30 billion to OpenAI’s latest funding round after reportedly considering a $100 billion investment previously.

Where next for Oracle?

On a more positive note, OpenAI is believed to now intend to spend $600 billion in compute by 2030, compared to its long-term target of $1.4 billion. It’s still a huge number, but the reported clarification on the timeline will help the market not pencil in even more aggressive, and less achievable, spending targets by 2030.

That should reduce investors’ risk somewhat. Still, Oracle and OpenAI have a lot further to go before fully convincing the market.

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, and Oracle. The Motley Fool has a disclosure policy.