I Predicted That ExxonMobil Would Join the $1 Trillion Club by 2030, But the Stock Is Already Up 24% in 2026. Is the High-Yield Dividend Stock Still a Buy Now?

- Finance

ThePostMaster

ThePostMaster- 0

- 10 minutes read

Energy stocks are in the spotlight, and ExxonMobil is best in breed.

The $1 trillion club continues to get bigger, with Walmart becoming the 10th U.S. company to surpass $1 trillion in market capitalization. It joins Nvidia, Alphabet, Apple, Microsoft, Amazon, Meta Platforms, Broadcom, Tesla, and Berkshire Hathaway. Eli Lilly has been in and out of the club, and JPMorgan Chase needs less than a 15% gain to reach $1 trillion.

I pegged ExxonMobil (XOM +2.62%), Visa, Oracle, and Netflix as dark horse candidates to reach $1 trillion by 2030. But ExxonMobil is off to the races so far this year — up 23.9% year to date at the time of this writing, pushing its market cap to $622.9 billion.

Here’s why ExxonMobil is soaring, and whether the high-yield dividend stock is still a buy now.

Image source: Getty Images.

A sectorwide rally

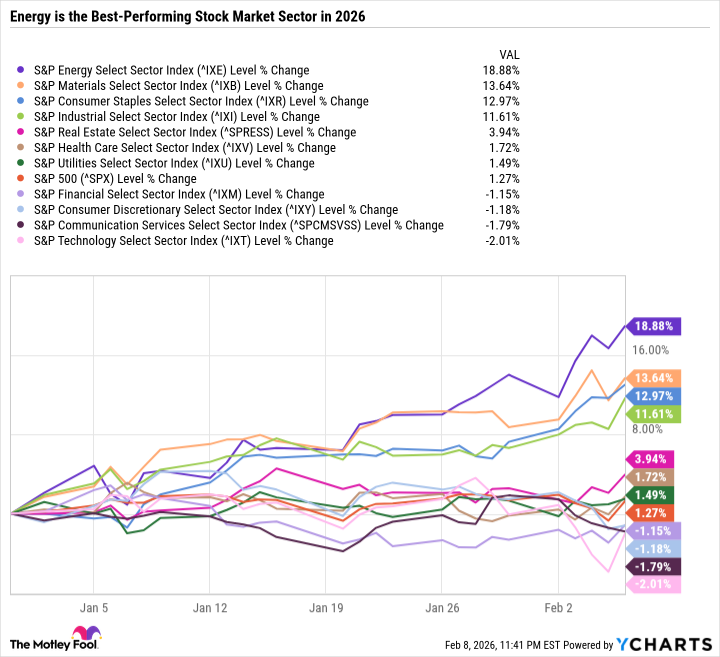

Energy has been the best-performing sector year to date, partly thanks to ExxonMobil, the sector’s largest component.

^IXE data by YCharts.

As you can see in the chart, other sectors that have done well are materials, consumer staples, and industrials. High-growth sectors like technology and communication services have lost value.

After a multi-year, rip-roaring rally in artificial intelligence (AI) growth stocks, investors are taking a pause this year by questioning elevated valuations and outsized AI spending. The skepticism is somewhat warranted, especially when you have a company like Amazon saying it’s going to spend $200 billion in 2026 capital expenditures, even though it only earned $139.5 billion in trailing 12-month cash from operations.

Today’s Change

(2.62%) $3.97

Current Price

$155.56

Key Data Points

Market Cap

$639B

Day’s Range

$153.57 – $156.93

52wk Range

$97.80 – $156.93

Volume

23M

Avg Vol

18M

Gross Margin

21.56%

Dividend Yield

2.64%

ExxonMobil is delivering results despite lower oil prices

ExxonMobil benefits from increased oil and gas demand from AI. But besides that, it is uniquely removed from the AI investment thesis. ExxonMobil has hard assets and a business model that is relatively insulated from AI. It stands out as a clear winner from AI, which can help improve operations and lower costs, rather than, say, a software company facing an existential threat.

ExxonMobil has a highly efficient production portfolio and expects to achieve 13% average earnings growth and double-digit cash flow growth per year through 2030. That guidance is based on mediocre oil prices — not on hoping that oil prices rise and lift margins.

ExxonMobil’s efficiency gains are largely thanks to its advanced assets, including its Permian Basin operations, liquefied natural gas, and offshore Guyana developments. These projects are particularly high-margin, and ExxonMobil expects them to account for 65% of its total 2030 oil-equivalent upstream volumes.

As an integrated oil and gas major, ExxonMobil also has significant investments in low-carbon technologies, such as carbon capture and storage. It also has a sizable refining and marketing business. That industry is doing very well due to higher refining margins.

In 2025, ExxonMobil’s energy products segment (which includes refining) grew earnings from $4.03 billion to $7.42 billion — an 84% increase. Lower oil prices dragged from ExxonMobil’s upstream earnings, which fell from $25.39 billion in 2024 to $21.35 billion in 2025, even though ExxonMobil produced 9.3% more oil equivalent barrels.

ExxonMobil remains a balanced buy

Even after its latest run-up, ExxonMobil is still a solid buy.

It’s a reliable dividend-paying value stock with 43 consecutive years of dividend raises, a 2.8% yield, and a reasonable 27.2 price-to-free cash flow (FCF) and 22.3 price-to-earnings (P/E) ratio.

That’s an elevated valuation from ExxonMobil’s 10-year median price-to-FCF of 20.6 and 10-year median P/E of 16.3. But ExxonMobil is arguably a far higher-quality company today.

JPMorgan Chase is an advertising partner of Motley Fool Money. Daniel Foelber has positions in Nvidia and Oracle and has the following options: short March 2026 $240 calls on Oracle. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Berkshire Hathaway, JPMorgan Chase, Meta Platforms, Microsoft, Netflix, Nvidia, Oracle, Tesla, Visa, and Walmart. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.