Could Change Following New Google-Backed Edge AI Coral Dev Board")

The sell-off in Oracle and Netflix is making aspirations to join the $1 trillion club increasingly distant.

In August, I predicted that Netflix (NFLX +1.58%) and Oracle (ORCL +3.01%) would reach at least $1 trillion in market capitalization by 2030. But Netflix is down 38.6% from its 52-week high at the time of this writing, while Oracle has fallen a staggering 56.5%.

Netflix’s market cap is now just $346.9 billion as I write this, and Oracle is at $410.4 billion — a far cry from joining Nvidia, Alphabet, Apple, Microsoft, Amazon, Broadcom, Meta Platforms, Tesla, Berkshire Hathaway, and Walmart on the list of U.S. companies with at least $1 trillion in market cap.

Here’s why both growth stocks are under pressure, and if they are still buys now.

Image source: Getty Images.

Oracle is raising capital to fund its AI spending

Like many software stocks, Oracle is undergoing a steep sell-off as artificial intelligence (AI) disrupts the once seemingly intractable moat of the software-as-a-service business model. But Oracle’s investments are mainly centered around building out data centers for Oracle Cloud Infrastructure (OCI), as well as multicloud data centers that embed its database service into third-party clouds like Amazon Web Services, Microsoft Azure, and Alphabet’s Google Cloud.

The market has become (rightfully) more skeptical about capital-intensive AI spending. Especially for companies like Oracle that are depending heavily on a handful of customers to fulfill order volume.

Oracle exited its most recent quarter with $99.98 billion in notes payable and other non-current borrowings (basically long-term debt) compared to just $19.24 billion in cash and cash equivalents.

On Feb. 1, Oracle announced a plan to raise $45 billion to $50 billion in gross cash proceeds in calendar year 2026 to fund the rapid expansion of OCI and meet contractual demand from companies like OpenAI, Nvidia, Advanced Micro Devices, Meta Platforms, TikTok, and xAI. The funding will come from a mix of selling at-the-market equity, convertible preferred securities, and bonds. None of these options is good, as the interest rate won’t be ideal on the bonds, and Oracle’s stock price is already so beaten down.

Taking on debt isn’t the worst thing in the world if a company is generating enough cash flow to pay it off. But Oracle reported negative $13.2 billion in free cash flow (FCF) in the second quarter of its fiscal 2026 compared to $9.5 billion in FCF in the same quarter from a year ago. Oracle has gone from being a high-margin cash cow to a capital-intensive money pit while it expands OCI. And that has investors worried that Oracle is betting too big on AI.

The silver lining is that spending should decline in the coming years as Oracle’s capital expenditures decrease and it starts realizing revenue from its backlog. But the company is highly vulnerable to a slowdown in AI spending.

If Oracle comes even remotely close to its forecast for $144 billion in fiscal 2031 (calendar year 2030) OCI revenue, the company will likely be worth far more than $1 trillion. But it could also continue underperforming the broader indexes if it doesn’t get its balance sheet under control.

Today’s Change

(3.01%) $4.71

Current Price

$161.19

Key Data Points

Market Cap

$450B

Day’s Range

$155.39 – $161.50

52wk Range

$118.86 – $345.72

Volume

567K

Avg Vol

29M

Gross Margin

65.40%

Dividend Yield

1.28%

Netflix stock is no longer priced at an ultra-premium

Unlike Oracle, which has legitimate issues challenging its investment thesis, Netflix is selling off mainly for valuation concerns and mixed reactions to its planned acquisition of Warner Bros. Discovery (WBD +0.05%).

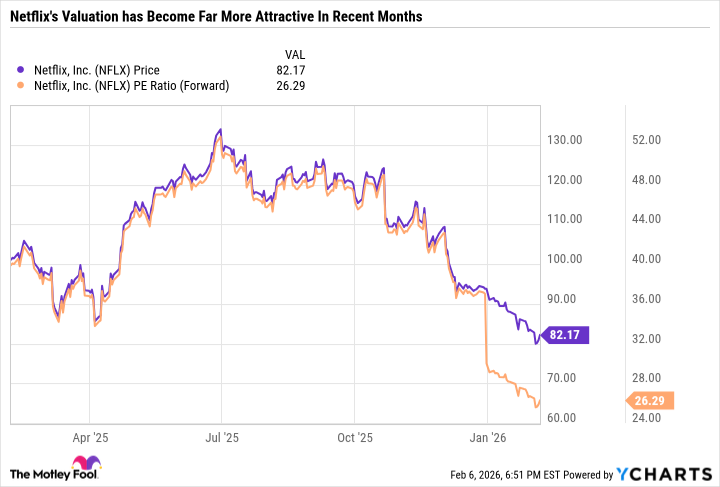

As you can see in the following chart, Netflix’s valuation has come down significantly since the stock peaked at a split-adjusted intraday high of $134.12 on June 30, 2025.

NFLX data by YCharts

Trading at just 26.3 times forward earnings, Netflix is within striking distance of the S&P 500‘s forward P/E of 23.6. But Netflix is a far better company than the typical S&P 500 component.

Netflix generates high margins and is growing at a solid rate. The company’s cash flow means it can fund its content spending without relying on debt, giving it a clear runway for compounding over time.

Netflix has had tons of success with both live-action and animated series and movies, from Stranger Things to its most successful film ever, KPop Demon Hunters.

Adding Warner Bros. Discovery assets would broaden Netflix’s content suite and allow it to pair HBO and HBO Max programming as a dual offering with Netflix or simply bundle it into a high-octane streaming subscription.

Warner Bros. is a smart acquisition, but Netflix doesn’t need it to succeed. Which is why the stock is still a buy even if the deal falls through.

Daniel Foelber has positions in Nvidia and Oracle and has the following options: short March 2026 $240 calls on Oracle. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Apple, Berkshire Hathaway, Meta Platforms, Microsoft, Netflix, Nvidia, Oracle, Tesla, Walmart, and Warner Bros. Discovery. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

, iShares Gold Trust Shares (ARCA:IAU)")