Impact of Florida Reforms ‘Undeniable,’ Reinsurance Should Drop Again

- Insurance

ThePostMaster

ThePostMaster- 0

- 13 minutes read

Adam Schwebach, broker and head of property for North America at Gallagher Re, the global reinsurance broker, last week sat down for an interview with Insurance Journal. The discussion came on the heels of Gallagher Re’s annual Florida broker summit, which provided some fresh insights into the shape of the reinsurance market and the continued impact of recent legislative reforms in the Sunshine State. The conversation has been lightly edited for clarity and brevity.

IJ: How was the Florida broker event this year?

AS: This was our 11th annual summit. This group consists of Florida carriers—we get a very good cross section of Florida-specific carriers—plus plenty of reinsurers. But also, other important stakeholders, including the Florida Office of Insurance Regulation, the Florida Cat Fund, Citizens (Property Insurance Corp.) are all there. It’s meant to set the stage leading into the 6/1 renewals, with topics that are important to the market.

With the litigation crisis that had plagued Florida for many, many years, we would get together in past years and there weren’t a lot of positives to talk about. If you look at the past couple of years, though, with the passage of the 2022 and 2023 (litigation reform) legislation, there’s been a market change in mood. I would say when that legislation passed there was a bit of skepticism from reinsurers. I think they told brokers and carriers at the time that it looked positive but they had also been promised in years past that legislation that was passed was going to really impact the market, and that wasn’t always the case. They were taking a more wait-and-see approach to the legislation to make sure it had the intended impact before they would give it full credit.

We never like to see hurricane events in Florida—I live there. With Milton and Helene, that was in my back yard, so we didn’t enjoy evacuating. But there are positives that come out of those situations as well. And one of those with Milton was that it created some really good test cases and the ability to compare that hurricane event with previous events and truly show that the legislation that was passed was transformative. It allowed carriers and reinsurers to become very, very comfortable with the exposures they had and the ability to assess the loss potential. The legislation was taking the uncertainty out of their models, the uncertainty around how much litigation could happen post-event.

If you had attended our summit in January 2025, I would have described the conversation as cautious optimism. Now, nearly 18 months after Milton, the proof is undeniable. As opposed to cautious optimism in 2025, we’ve removed the caution. What we’re hearing from reinsurers is that they are actively and proactively taking a look at some of the assumptions that they previously had included in their underwriting and pricing processes, such as litigation and social inflation, that was a driver of the cost of their reinsurance. They’re reviewing that now and absolutely looking for ways to reduce those types of loads, which is going to have a very positive impact on renewals this year.

IJ: What are your predictions on the June 1 renewals, compared to Jan. 1?

AS: Jan. 1 saw rate reductions; we would expect the same going into the mid-year renewals. The one difference is that we are hearing and seeing that reinsurers are able to proactively review some of the pricing assumptions they were making. I’m not sure they have the same ability throughout the rest of the U.S. and the global reinsurance environment to actively look at reducing loss costs (like Florida has). A carrier or broker may give a headline number, but a reinsurer may see that they’ve actually reduced loss costs. The brokers and carriers may think rates are down “X” amount; the reinsurer may say that, because of reduced loss costs, it’s something less than “X.” I think it’s a good outcome for reinsurers and for the market as a whole.

IJ: Over the last decade, how much have reinsurance rates changed in Florida?

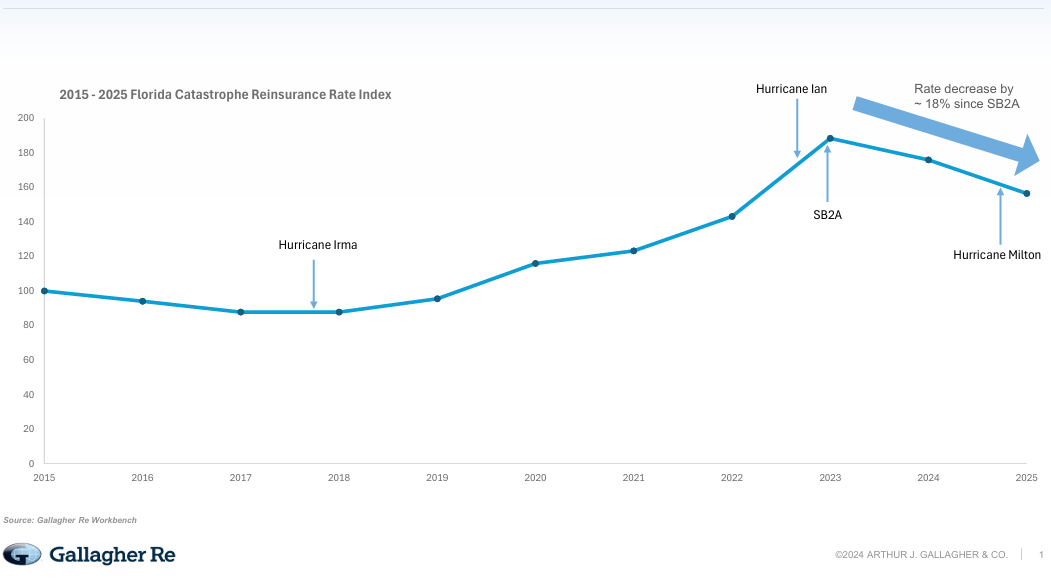

AS: We have a rate online index. (See chart provided by Gallagher Re, below.) A low-water-mark was 2017-2018 and after that. Overall, rates are still elevated from that time but much less so than they were in 2022, when the litigation crisis was peaking.

IJ: The big question now, with rates moderating, are Florida capacity levels balanced, or is the supply of reinsurance now exceeding demand, in your view?

AS: There are a couple of variables that we’re mindful of going into this year. The depopulation of Citizens is going to take some of the reinsurance purchases away from Citizens and move that to the primary market. Citizens buys slightly differently from the rest of the market. They don’t buy anything below the Cat Fund, whereas the rest of the market will need to. That will create some additional demand at the bottom end of a reinsurance tower. Everything we have reviewed tells us that there is ample supply of reinsurance at those levels. We’re absolutely seeing reinsurers willing to consider moving down in reinsurance programs, where during the litigation crisis they were looking to move up to get away from those types of layers. Given the legislative changes, there’s a willingness to move further down in programs, which increases the supply.

At the top end of programs, nothing’s infinite, but in our mind there’s a seemingly endless supply of capacity for the traditional market and what’s driven by the ILS (insurance-linked securities) market to write that less-exposed, higher-end limit in programs. The cat market, the ILS market is truly driving supply in that market and putting pressure on the traditional market in that regard.

IJ: Speaking of the Florida Cat Fund (the Florida Hurricane Catastrophe Fund or FHCF): Every year there’s talk about lowering the retention for the fund. It seems unlikely to pass this year, but do reinsurers have questions about that?

AS: It’s something that has come up a fair bit recently. Over the past year or so, if the FHCF is presenting at an event, someone is going to raise their hand and ask that question. It seems like there’s definitely some appeals from the carrier side—but not from all—that it would be helpful if the FHCF would consider it. Seems like there’s a hesitation from the fund in doing that, and probably rightly so. The FHCF as it’s currently structured and where it sits in reinsurance programs is doing exactly what it was made to do—providing significant amounts of reinsurance and stabilizing the market. The FHCF, having never needed a dollar of budgetary funding from the state of Florida, has to be one of the absolute largest success stories in terms of what it has stabilized and has helped create a vibrant Florida insurance market. When the market is hard, you hear more about that.

IJ: Can you talk a little more about the impact that Citizens’ depopulation and the presence of so many more carriers in the Florida market in the last year has had on reinsurance?

AS: By and large, the supply of reinsurance is absolutely there. Some of the new carriers are existing carriers that were restructured. Those are elements that can limit demand, but I think the reinsurance market has stepped into that. It’s good timing, if the reinsurance market is softening, to bring new carrier opportunities. On the flip side, it has a very positive impact on the primary market as well. Citizens shrinking to the level it’s at is good for every policyholder and everyone in Florida. I think people forget about the assessment potential with Citizens but when Citizens is over 1 million policies, there is an unknown assessment probability that could impact everybody. At their current level, under 400,000 policies, and with their surplus levels, that assessment probability is so vastly reduced that it’s good for everybody in the state.

IJ: Where do you see the reinsurance market in Florida in, say, five years? Are all signs pointing to a bright future?

AS: I think so. I think the hope and goal of all stakeholders right now should really be stability. Stability leads to natural competition and improvement for policyholders, for carriers and for reinsurers, all the way around. I would give a ton of credit to the governor’s office, legislators and the Office of Insurance Regulation who, over the past year have done a wonderful job of getting in front of the various reinsurance stakeholders and making sure they understand that the reforms that were passed are not going anywhere. That’s incredibly important to the market—maintaining stability.

Even last year, there were some bills that were looking to repeal aspects of the reforms. That has an impact. As reinsurers are reading those reports and seeing that legislation, that does cause them uncertainty. And the one thing reinsurers are good at is they can price for uncertainty. It’s just expensive. To the extent that the uncertainty is not part of the conversation this year, that leads to long-term stability. My hope is that the longer these reforms are in place, and we expect that to be many, many years, we do get to a point where reinsurance becomes a non-issue in the state. That’s the ideal outcome.

If reforms continue to operate as intended and reinsurers are giving credit for reduced risk in their pricing, and those savings are being passed on to policyholders, you get to a point where, in conversations with friends and neighbors, it just doesn’t come up anymore because there are ample options and ample capacity for policyholders to have options and feel protected.

IJ: Last year was a pretty quiet hurricane season for Florida. Are reinsurers worried that things could change this year or next with maybe two big storms in one season?

AS: We have our chief science officer who hosted some webinars with Colorado State University and others. I’ve been reminded that it was a quiet year from a landfall perspective but there were plenty of hurricanes in the Atlantic. We dodged some bullets and nothing made landfall. But I think it’s in the back of everyone’s mind that we live in a peninsula that juts out into very warm water. Hurricanes will happen. I think what we will see going into this renewal is, while the carriers are extremely comfortable and have been able to purchase levels of reinsurance that meet their risk-transfer goals and tolerances, we could see some carriers take their reinsurance cost savings to buy more coverage. Whether that’s multiple-events coverage—I think everyone remembers 2004 and 2005 when there were four events that impacted the state—or aggregate coverage that was not available before, all of those are potential conversations carriers will be looking to have with reinsurers.

Also, we’re seeing more and more of that type of structural innovation being included in cat bond offerings, which is a positive for our clients that are accessing that form of capital. It’s something the traditional market may need to more avidly consider, if only to match what the cat bond market is doing.

From 2025: Florida Reinsurance Buyers Found Ample Property Capacity at Mid-Year Renewals

Topics

Florida

Reinsurance