-2%20(1).avif?ssl=1 "I Want to Talk About Shopping Addiction (Again)")

Artificial intelligence (AI) has been a tailwind for cloud computing companies, which allow their clients to run AI workloads without investing in expensive hardware, and DigitalOcean (DOCN +3.39%) has been one of the beneficiaries of this business model.

While there are major cloud computing companies such as Amazon, Microsoft, Alphabet, and others renting out data center capacity to customers so they can build, customize, and run AI models and applications, DigitalOcean has carved out a niche in serving smaller customers. It operates an on-demand cloud infrastructure platform for start-ups and growing technology companies.

DigitalOcean also offers platform-as-a-service (PaaS) and software-as-a-service (SaaS) solutions that make it easier for customers to create and use AI applications. Its business model is proving successful, as is evidenced by its latest results.

Here’s why DigitalOcean is a top growth stock you can buy right now, even if you have just $60 in investible cash.

Image source: Getty Images.

DigitalOcean’s growth is poised to accelerate

DigitalOcean released its fourth-quarter and full-year results on Feb. 24. Its revenue increased by 15% in 2025 to $901 million. Importantly, management expects stronger growth of 21% in 2026 and 30% in 2027.

Today’s Change

(3.39%) $1.84

Current Price

$56.10

Key Data Points

Market Cap

$5.2B

Day’s Range

$51.05 – $56.33

52wk Range

$25.45 – $70.43

Volume

106K

Avg Vol

2.7M

Gross Margin

59.86%

Management made it clear on the earnings call that AI is playing a central role in powering its growth. DigitalOcean’s annual run-rate revenue (ARR) from AI-specific customers increased by an impressive 150% year over year in the fourth quarter to $120 million. That was significantly higher than its overall ARR increase of 18% to $970 million.

DigitalOcean points out that its AI customers are not just renting computing capacity from its data centers; they’re also building and scaling applications on its platform. For instance, the ARR for AI inference services increased by a whopping 254% in the quarter.

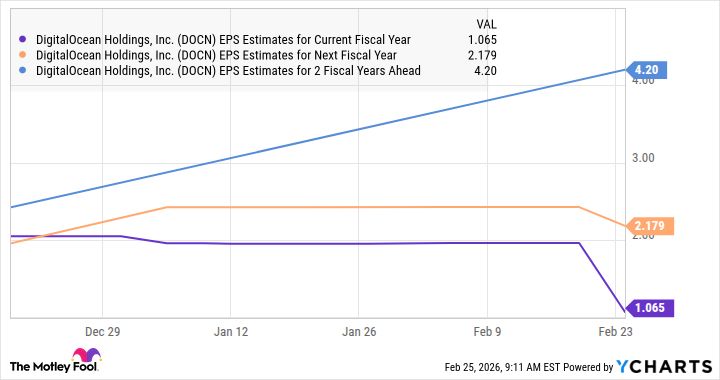

The full-stack nature of DigitalOcean’s AI platform, which offers both hardware and software to customers, should be a tailwind for the company’s bottom line, enabling it to generate more revenue and build a strong recurring revenue stream. This is probably why analysts are anticipating a sharp rise in the company’s earnings over the next couple of years.

DOCN EPS Estimates for Current Fiscal Year data by YCharts.

Incremental investments in data centers and graphics processing units are likely to weigh on DigitalOcean’s bottom line, as management indicated on the conference call. That’s probably why analysts have lowered their earnings estimates for 2026 and 2027. However, the software-centric AI services it offers should eventually help it generate more sales and boost the bottom line.

The stock is a no-brainer buy right now

DigitalOcean’s stock jumped by nearly 6% after it reported its latest results, but in the days since, it has given those gains back, and now trades at under $60 a share. So, if you have $60 to invest right now, this AI stock looks like an ideal bet since it trades at an attractive 26 times forward earnings.

Assuming DigitalOcean can indeed deliver the healthy earnings growth that analysts expect by 2028 and continues to trade at 26 times earnings at that time (almost in line with the tech-laden Nasdaq-100 index’s forward earnings multiple), the stock could jump to $109.

That suggests a potential upside of about 95% within the next three years, which is why it would make sense to buy DigitalOcean before it soars higher.