Just a few years ago, Google Cloud Platform (GCP) was a quiet punchline in Alphabet‘s (GOOGL +2.59%) (GOOG +2.47%) portfolio: A cash-burning experiment that most investors overlooked while Amazon Web Services (AWS) and Microsoft Azure dominated cloud computing budgets.

Then artificial intelligence (AI) changed the narrative entirely. What was once an also-ran became one of Alphabet’s fastest-growing, most profitable divisions. At the end of the first quarter, GCP boasted a backlog of more than $460 billion.

This is more than just a headline number. It is validation that large enterprises and leading AI developers are voting with their wallets — signaling a shift in cloud market dynamics that makes Alphabet stock a standout long-term opportunity even after its recent run.

Image source: Getty Images.

Google Cloud’s turnaround

Despite infusions of meaningful capital into cloud infrastructure, GCP consistently posted mundane revenue figures and piled up operating losses while competitors generated double-digit growth and healthy margins. Indeed, enterprise customers were slow to migrate to GCP as they were drawn to AWS’s maturity or Azure’s integration with ChatGPT.

By the first quarter of 2026, however, GCP was not only achieving consistent profitability but delivering the kind of growth that once seemed impossible: revenue surging past $20 billion in a single quarter, up more than 60% year over year. Meanwhile, operating income more than tripled.

This shift was not driven by cost-cutting efforts or savvy marketing campaigns. Rather, Google Cloud’s renaissance comes from a fundamental repositioning that places AI at the center of the platform — turning each layer of compute infrastructure into something purpose-built for the intelligence economy.

Today’s Change

(2.59%) $10.04

Current Price

$397.39

Key Data Points

Market Cap

$4.7T

Day’s Range

$385.00 – $397.96

52wk Range

$159.61 – $402.00

Volume

497K

Avg Vol

30M

Gross Margin

60.43%

Dividend Yield

0.22%

AI is GCP’s secret sauce

Alphabet’s leadership realized that the future of cloud services would not be won on storage or basic compute alone. Rather, next-generation cloud infrastructure needs to provide the ability to train, deploy, and scale advanced AI systems.

The cornerstone of Google Cloud is Alphabet’s Gemini Enterprise Agent Platform, a unified environment that allows customers to build, govern, and optimize AI agents at scale. Moreover, Google’s custom tensor processing units (TPUs) deliver optimal price-performance for both training and inference, often outperforming generic GPUs in certain tasks while consuming less energy.

These technical edges have translated into landmark commercial victories with marquee AI labs. Anthropic alone is rumored to be doubling down on its existing relationship with GCP, this time in a $200 billion commitment over five years. Meanwhile, OpenAI, which has been historically tied to Azure, quietly expanded its footprint across multiple clouds after allocating workloads to GCP precisely because of its specialized AI silicon and software stack combination.

GCP’s flywheel effect is now undeniable: One successful AI deployment fuels rapid expansion across the entire organization, often pushing capex spend well above initial agreements.

GCP’s backlog signals an acceleration in cloud market share

In my eyes, Google Cloud’s $460 billion backlog is the clearest signal yet that the platform is not just a participant in the AI boom but rather turning into a leader in a segment that increasingly matters as AI workloads expand.

GCP’s 63% revenue growth now dwarfs Azure’s roughly 40% and AWS’s 28%, suggesting the former laggard is gaining market share fast. While AWS retains overall market leadership and Azure enjoys a high level of ecosystem lock-in, GCP is starting to win the battle for more defining workloads.

The multi-cloud strategies employed by the likes of OpenAI and Anthropic reinforce the trend. Organizations with deep primary partnerships are swiftly diversifying into GCP to tap its strengths and differentiators — validating the reality that no single provider can satisfy all customer demands in the AI economy.

Despite Alphabet stock’s recent momentum and valuation expansion, GCP’s trajectory makes the stock a compelling long-term buy. The backlog provides rare forward visibility — hundreds of billions of dollars already contracted and set to convert steadily into recognized revenue throughout the AI infrastructure era.

Profit margins are still expanding as AI services scale, and the current capital expenditure (capex) cycle, while substantial, is not speculative. It is simply required to fulfill the contracted demand. Once this capacity comes online, incremental revenue growth should flow to the bottom line at notably high margins. Meanwhile, Alphabet’s core businesses — Search, YouTube, and subscription services — continue to throw off enormous cash flow that helps subsidize the AI buildouts.

Through Alphabet stock, growth investors are buying a diversified technology ecosystem whose fastest-growing segments remain in the early innings of a multiyear AI-driven supercycle.

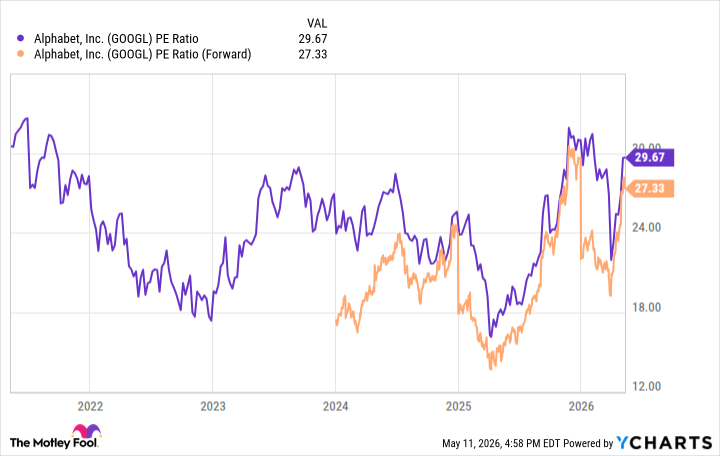

GOOGL PE Ratio data by YCharts

While the valuation may look priced to perfection on the surface, the locked-in growth path suggests the market has not yet fully baked in how GCP’s accelerating backlog will translate into sustained earnings power. For patient investors, GCP’s improbable rise is more than an inspiring story. It is the core pillar supporting Alphabet stock as one of the most attractive mega-cap compounders in the market today.