Stock: Amazon vs. Alphabet")

Two of the big-four artificial intelligence (AI) hyperscalers are Alphabet (GOOG +3.34%) (GOOGL +3.15%) and Meta Platforms (META +2.70%). These two are major brands and have captured the attention of the market.

However, one thing sets Meta Platforms apart from the other three hyperscalers, and it’s not a good thing. Recently, Meta reportedly took steps to remedy this difference, and investors may learn more about it during its upcoming earnings announcement.

But does that make it a better buy than Alphabet? Let’s take a look.

Image source: Getty Images.

Meta Platforms currently doesn’t have a cloud computing business

All of the big four AI hyperscalers are spending hundreds of billions of dollars on AI data centers this year. Still, only Meta Platforms uses all of it for internal computing purposes. The other three have cloud computing businesses where they rent out computing capacity on their servers. That’s a big deal because the other three have a valid revenue-generating engine in addition to what they’re doing internally.

So, if their AI efforts turn out to be a flop, they can at least sell that computing capacity to those winning the AI arms race. Meta has gone all-in on its internal AI, and there really hasn’t been a lot to show for it. The concern here is that Meta’s AI spending is like the metaverse 2.0, where it spent billions of dollars for no return on investment.

However, that could be changing. CEO Mark Zuckerberg said a while back that Meta might consider forming a cloud computing business if it had excess computing capacity. However, according to reports, Meta is set to start forming this business. This is music to investors’ ears, as it finally gives investors a tangible payoff for the massive amount of money being spent on data centers.

Today’s Change

(2.70%) $17.86

Current Price

$678.90

Key Data Points

Market Cap

Day’s Range

$656.75 – $686.00

52wk Range

$520.26 – $796.25

Volume

904K

Avg Vol

17.9M

Gross Margin

81.94%

Dividend Yield

0.32%

Alphabet is already involved in this space with Google Cloud, and its growth rates have been explosive. In Q2, its cloud business generated more than $20 billion in revenue and had a 33% operating margin, so it’s clearly a lucrative business to be in. But that’s only one part of Alphabet’s business. How does the rest stack up?

Meta is still growing faster than Alphabet without cloud computing

At their core, both Meta and Alphabet are advertising companies. Meta makes its ad revenue through its social media platforms like Instagram, Facebook, WhatsApp, and Threads. Alphabet’s ad revenue comes from its Google family of products and YouTube. During Q1, Alphabet’s revenue rose 22% year over year. Meta’s growth was faster, coming in at 33% year over year. Both companies have utilized their AI resources to implement new technologies to better convert on advertising, which helped boost each business’s revenue.

Today’s Change

(3.15%) $11.33

Current Price

$370.84

Key Data Points

Market Cap

Day’s Range

$357.78 – $373.64

52wk Range

$180.48 – $408.61

Volume

852.4K

Avg Vol

31.3M

Gross Margin

60.43%

Dividend Yield

0.24%

But if Meta can create a booming cloud business that rivals Google Cloud, then its growth rate could push even higher. Meta’s growth has more potential and is currently faster than Alphabet’s. As a result, I’m giving Meta the win in the growth category.

Winner: Meta Platforms

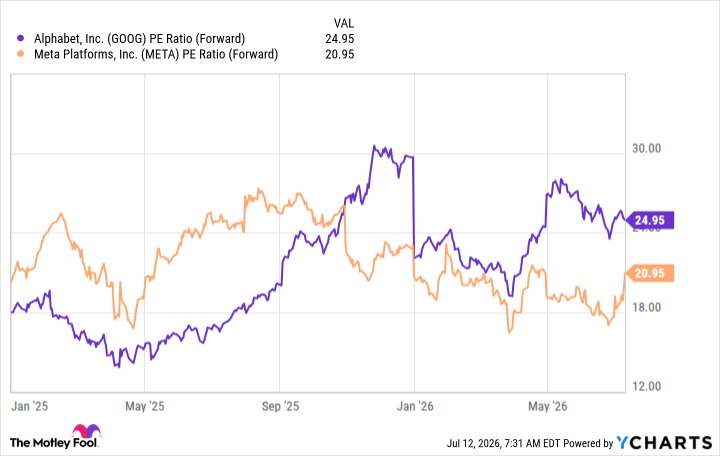

Alphabet trades at a premium

From a valuation perspective, Meta trades at a decent discount to Alphabet. At 25 times forward earnings, Alphabet is a typically valued big tech stock and isn’t undervalued or overvalued. At nearly 21 times forward earnings, Meta still trades at a discount to the S&P 500 (valued at 21.7 times forward earnings).

GOOG PE Ratio (Forward) data by YCharts

Should Meta announce and implement a solid cloud computing business, I could see it closing the gap easily over the next few months. That would lead to soaring returns, making it a solid stock to buy now. As a result, it gets the nod here as well.

Winner: Meta Platforms

Meta has more upside, but it still may not be the stock for you

Meta Platforms’ potential upside is far greater than Alphabet’s — if everything works out. If it decides not to launch a cloud computing business or struggles to do so, Meta’s stock may sell off to lower levels again. There isn’t a ton of execution risk right now with Alphabet; it’s at the top of its game and excelling in every area.

If you want ultimate upside, then Meta is the stock for you. If you want solid, market-beating returns with less risk, then Alphabet makes for a better stock.