With a $5.2 trillion market capitalization, Nvidia (NVDA +1.90%) is the world’s largest company. It supplies the most widely used graphics processing units (GPUs) for data centers, which are the main chips used to power artificial intelligence (AI) development. Demand for this hardware is still growing rapidly, and currently far exceeds supply.

With a market cap of $4.8 trillion, Alphabet (GOOG 2.62%)(GOOGL 2.98%) is the world’s second-largest company. It operates an incredibly diverse portfolio of tech businesses, including Google Search, Google Cloud, YouTube, and Waymo. The company has even entered the market for data center processors in an attempt to compete with Nvidia.

Looking ahead, which one of these companies is more likely to achieve a $10 trillion valuation first?

Image source: Getty Images.

The case for Nvidia

Nvidia’s GB300 data center GPU is one of the most sought-after AI chips in the world right now. It’s based on the company’s Blackwell architecture, and in certain configurations, it delivers up to 50 times more performance than the company’s Hopper-based H100 GPU, which hit the market in 2022. But Nvidia will up the ante again in the second half of this year, when it starts shipping commercial quantities of its new Vera Rubin platform.

Vera Rubin includes the Rubin GPU, the Vera central processor (CPU), and upgraded networking equipment. Nvidia says customers who adopt the platform will be able to train AI models using 75% fewer GPUs, which will reduce the cost of AI inference tokens by 90%.

In other words, Vera Rubin will substantially lower the cost of deploying AI software, which should lead to wider adoption of such software — and, therefore, higher demand for Nvidia’s chips. The company is banking on this flywheel effect to dramatically increase infrastructure spending among some of its biggest data center customers, which include OpenAI, Anthropic, Alphabet, Amazon, Microsoft, and Meta Platforms.

Today’s Change

(1.90%) $4.08

Current Price

$219.28

Key Data Points

Market Cap

$5.3T

Day’s Range

$213.89 – $222.30

52wk Range

$124.47 – $222.30

Volume

58K

Avg Vol

171M

Gross Margin

71.07%

Dividend Yield

0.02%

Nvidia’s total revenue rose 65% year over year to $215.9 billion in its fiscal 2026 (which ended Jan. 25). But Wall Street is anticipating that its growth will accelerate to 71% in fiscal 2027, with revenue expected to come in at $370 billion, according to Yahoo! Finance. This highlights the company’s incredible momentum.

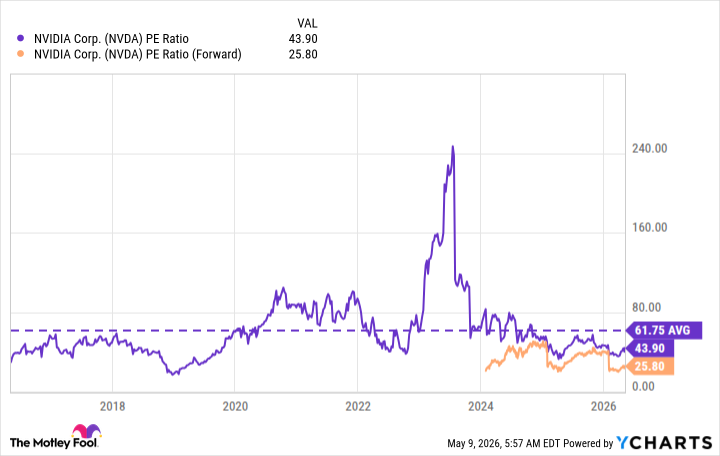

In my opinion, Nvidia has a clear line of sight to a $10 trillion market cap. Based on the company’s adjusted (non-GAAP) earnings of $4.77 per share, its stock is trading at a price-to-earnings (P/E) ratio of 43.9. But it’s trading at a forward P/E of just 25.8 based on Wall Street’s expectations for fiscal 2027.

NVDA PE Ratio data by YCharts

However, Nvidia’s 10-year average P/E is 61.7. Its stock would have to soar by 139% over the next 12 months just to trade in line with that average, which would result in a market cap of $12 trillion.

The case for Alphabet

When the AI boom started picking up steam in early 2023, investors were worried it would hurt Alphabet because chatbots were providing a convenient new way to find information online that didn’t involve traditional search engines such as Google Search. But the company has blown those concerns to smithereens by strategically using AI to improve its search experience.

Using its powerful Gemini large language models as a foundation, Alphabet created two new features for Google Search called AI Overviews and AI Mode. Overviews combine text, images, and links to third-party sources to craft direct answers to user queries, while clicking on AI Mode transfers users to a chatbot-style interface where they can enter follow-up questions and dive deeper.

Alphabet says these features are fueling overall search growth. In fact, Google Search produced a record $60.4 billion in revenue during the first quarter. That was a 19% increase from the year-ago period, and it was the fourth consecutive quarter in which that growth rate accelerated.

Today’s Change

(-2.98%) $-11.94

Current Price

$388.86

Key Data Points

Market Cap

$4.7T

Day’s Range

$388.76 – $397.42

52wk Range

$156.16 – $402.00

Volume

18K

Avg Vol

30M

Gross Margin

60.43%

Dividend Yield

0.22%

Google Cloud is another one of Alphabet’s booming AI businesses. It operates data centers powered by the latest chips from suppliers such as Nvidia and rents the computing capacity to enterprises. However, Alphabet just unveiled its eighth-generation Tensor Processing Unit (TPU), which it designed as an alternative to Nvidia’s GPUs. The 8t, for AI training, offers three times more processing power than the company’s previous TPU, while the 8i, for AI inference, delivers up to 80% better performance-per-dollar than its predecessor.

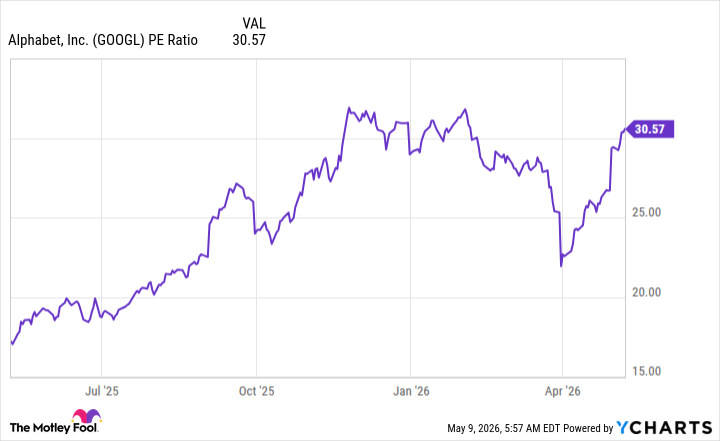

From a valuation perspective, Alphabet stock is trading at a P/E ratio of 30.5. That is a slight discount to the average P/E of the Nasdaq-100, which is currently 35.6, suggesting Alphabet is undervalued relative to its big-tech peers.

GOOGL PE Ratio data by YCharts

However, even with a little bit of “multiple expansion” (a higher P/E ratio), Alphabet would still have to nearly double its earnings to justify a market cap of $10 trillion. That could take a few years, even in the AI era.

The verdict

Based on the facts at hand today, I think Nvidia will beat Alphabet in the race to the $10 trillion milestone. But there is a caveat. The semiconductor industry has historically been very cyclical, in part because companies would only invest heavily to upgrade their data center infrastructure once every few years. The AI revolution has compressed the upgrade cycle to 12 months, and in some cases even less, but this requires a frankly unsustainable pace of spending from some of Nvidia’s top customers.

If their spending on data center infrastructure starts to slow, investors won’t feel comfortable paying a high P/E multiple for Nvidia stock, which could send its market cap tumbling.

Therefore, while Nvidia looks more likely to achieve a $10 trillion valuation first, I think Alphabet has a better chance of maintaining that kind of market cap over the long run. It has a more diversified business, and its P/E ratio consistently trades in line with or below the P/E of the Nasdaq-100, which is far more sustainable.